Family Waqf (Waqf Zuhri): Reimagining Wealth, Responsibility, and Legacy in Muslim Societies

In most modern conversations about wealth, the focus is strikingly narrow. We speak about accumulation, returns, diversification, and, at best, intergenerational transfer through inheritance. Yet, within the Islamic tradition, wealth was never meant to be understood only as private property. It was framed as a trust (amānah) something to be managed with accountability, purpose, and continuity beyond one’s lifetime.

One of the most sophisticated institutional expressions of this worldview is waqf. And within it, one form remains particularly misunderstood today: family waqf (waqf zuhri or waqf ahli).

This article revisits the concept not as a historical artifact, but as a strategic financial and social instrument one that may be deeply relevant in an age of fragile family structures, wealth inequality, and short-term financial thinking.

What Is Family Waqf?

Family waqf refers to an endowment established by an individual where the primary beneficiaries are the founder’s family or descendants, while ultimately retaining a charitable dimension.

Unlike a standard charitable waqf, where benefits are directed immediately toward public causes, a family waqf creates a structured flow of benefits across generations, often with conditions attached such as education, maintenance, or welfare of descendants.

Importantly, ownership of the endowed asset is transferred permanently to Allah, meaning it cannot be sold, inherited, or disposed of. Only its usufruct (benefits) is distributed.

As noted in classical and contemporary literature, waqf represents a mechanism that combines private intention with public good, ensuring both family protection and long-term societal contribution (Kahf, 1998).

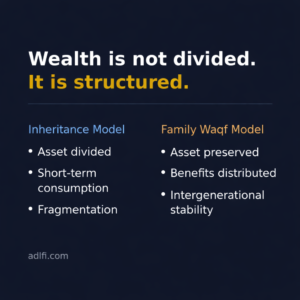

Beyond Inheritance: A Different Logic of Wealth

Modern inheritance systems even when Islamically compliant tend to focus on division of assets. Wealth is fragmented across heirs, often leading to:

- Dissipation of capital

- Family disputes

- Loss of long-term economic stability

Family waqf introduces a fundamentally different logic.

Instead of dividing assets, it preserves the asset base while distributing benefits over time. This creates:

- Intergenerational financial stability

- Protection against reckless consumption

- A structured governance framework within families

In economic terms, this resembles a perpetual family trust, but with a moral and spiritual foundation that extends beyond legal structuring.

Kuran (2001) argues that historically, waqf institutions played a central role in shaping economic and social organization in Muslim societies, particularly in sustaining long-term asset continuity.

The Governance Dimension: Discipline Within the Family

One of the most overlooked aspects of family waqf is governance.

A well-structured waqf includes:

- A mutawalli (trustee) responsible for management

- Clearly defined beneficiary rules

- Conditions for distribution

- Succession mechanisms

This introduces discipline into family wealth management, something that modern financial systems often fail to enforce.

Rather than wealth being passively inherited, beneficiaries are often required to meet certain criteria such as pursuing education, maintaining ethical conduct, or contributing to the family structure.

In this sense, family waqf is not just a financial tool. It is a character-building institution.

Misconceptions and Historical Criticism

Family waqf has not been without criticism.

Some scholars and policymakers have argued that it:

- Concentrates wealth within families

- Limits economic circulation

- Can be misused to avoid inheritance laws

These concerns led to restrictions or abolishment of family waqf in several jurisdictions during the 20th century.

However, more recent scholarship suggests that these critiques often emerged from mismanagement and regulatory gaps, rather than inherent flaws in the model itself (Çizakça, 2011).

When properly governed, family waqf can balance:

- Private family welfare

- Long-term asset preservation

- Eventual public benefit

Why Family Waqf Matters Today

The relevance of family waqf today is perhaps stronger than ever.

We are living in a time where:

- Families are increasingly fragmented

- Wealth is consumed faster than it is built

- Financial planning is short-term and reactive

At the same time, Muslim professionals particularly in diaspora contexts like Canada are accumulating wealth without structured frameworks for Islamically aligned legacy planning.

Family waqf offers a compelling alternative:

- It protects children without fostering dependency

- It aligns wealth with purpose

- It creates continuity beyond one generation

In modern financial language, it functions as:

- A risk management tool

- A legacy planning instrument

- A values-based governance system

From Private to Public: The Built-In Transition

One of the unique features of family waqf is that it is rarely purely private.

In many structures, once family lines diminish or conditions are fulfilled, the waqf transitions toward public charitable purposes.

This ensures that wealth is not indefinitely locked within a family, but eventually contributes to broader societal welfare education, healthcare, or poverty alleviation.

This dual nature reflects a deeper Islamic principle:

Wealth serves both individual responsibility and collective good.

Reimagining Family Waqf in Modern Contexts

The challenge today is not whether family waqf is relevant but how it can be redesigned for contemporary realities.

Key considerations include:

- Legal compatibility within non-Muslim jurisdictions

- Professional asset management

- Transparent governance structures

- Integration with modern financial instruments

There is also potential to connect family waqf with:

- Islamic fintech platforms

- ESG and impact investing frameworks

- Cross-border asset structures

This is where scholars, practitioners, and policymakers need to collaborate not to replicate historical models blindly, but to rebuild them intelligently.

Perhaps the most important shift that family waqf invites is not technical, but philosophical.

It asks a different question:

Not “How much can I leave behind?”

But “What structure can I build that continues to benefit others after I am gone?”

In that sense, waqf is not merely about charity.

It is about continuity, responsibility, and intentional design of wealth.

And in a world driven by immediacy, that may be its most radical feature.